Table of Contents

DepEd, GSIS MOA to improve financial standing of indebted teaching, non-teaching personnel

In constantly promoting the welfare and improving the financial capability of its teaching and non-teaching personnel, the Department of Education (DepEd) today formalized its partnership with the Government Service Insurance System (GSIS) on the GSIS Financial Assistance Loan to DepEd Personnel (GFAL) during a ceremonial signing of the memorandum of agreement (MOA) at Malacañang.

Witnessed by no less than President Rodrigo Roa Duterte, Education Secretary Leonor Magtolis Briones and GSIS President and General Manager Jesus Clint Aranas signed the MOA on behalf of their respective agencies.

“This partnership is one way for DepEd to help hundreds of thousands of its teachers and personnel free themselves from the burden of loans and over-borrowing, while ensuring the preservation of their GSIS benefits and fulfilling DepEd’s legal mandate under the General Appropriations Act (GAA),” the Secretary reiterated.

GFAL is a financial assistance loan program extended by GSIS to eligible DepEd borrowers on a voluntary basis to help protect them from the risk of losing their hard-earned retirement or separation benefits.

Under GFAL, eligible DepEd borrowers’ existing loans with PLIs will be refinanced by the GSIS at a lower nominal interest rate of 6% per annum and a longer loan term of up to six years. Eligible DepEd borrowers who opt to avail of the GFAL will now be able to have reduced monthly loan amortizations. DepEd and GSIS have agreed to prioritize borrowers whose monthly payment for obligations exceed the P5,000 monthly NTHP to allow them to service their current obligation.

However, the Secretary emphasized that GFAL is voluntary and still gives DepEd borrowers the option to make their own restructuring arrangement with PLIs.

The MOA supports the DepEd Order No. 5, series 2018, which strictly implements the P5,000 minimum monthly NTHP of DepEd teachers and personnel.

POLICY AND PROCEDURAL GUIDELINES (PPG) NO. 327-18

GSIS FINANCIAL ASSISTANCE LOAN DEPARTMENT OF EDUCATION PERSONNEL (GFAL) TO (DEPED)

I. BACKGROUND

The 2014-2016 collection efficiency report (covering loans) of the GSIS shows that DepEd is the agency sector with the lowest collection efficiency on loans, averaging to 88% for DepEd and 62% for DepEd-ARMM, during the 3-year period:

| Agency Type | Jan-Dec 2014 | Jan-Dec 2015 | Jan-Dec 2016 |

|---|---|---|---|

| % | % | % | |

| DepEd | 88 | 89 | 88 |

| NGAs | 97 | 98 | 99 |

| LGU | 88 | 93 | 95 |

| GOCC | 97 | 99 | 99 |

| GFIs | 100 | 102 | 102 |

| Judiciary | 102 | 101 | 101 |

| Military | 92 | 98 | 98 |

| Pensioners | 102 | 102 | 100 |

| DepEd ARMM | 50 | 69 | 67 |

The deficiency in the net take home pay of DepEd personnel is one of the major causes of DepEd’s low collection efficiency. Efforts have been made to ensure that GSIS loans are prioritized over those from lending institutions; however, DepEd continued to queue GSIS loans together with the other loans of teachers.

It has also been a practice of DepEd to consider loan renewals as new loans, thus, collection of its first monthly installment will be queued with the rest of deductibles from the DepEd personnel’s salary, when it should be given priority as it is already a loan renewal.

Despite the stricter guidelines implemented in the Enhanced Conso-Loan Plus Program and the retrainings given to DepEd Agency Authorized Officers (AAOs) in which they are constantly reminded to prioritize in salary deductions all monies due the GSIS (premiums and loans), DepEd continued to lag behind in terms of timely and accurate remittance of loan repayments to GSIS. GSIS loans continued to be queued with the other loans of teachers.

On 31 July 2017, DepEd issued DepEd Order (D.O.) No. 38, s. 2017, to further clarify the implementation of the Php4,000 Net Take-Home Pay for its personnel pursuant to Section 47 of the General Provisions of the 2017 General Appropriations Act (GAA), to wit:

Section 47. Authorized Deductions. Deductions from salaries and other benefits accruing to any government employee, chargeable against the Personnel Services, may be allowed for the payment of an individual employee’s contributions or obligations due the following, and in the order of preference stated below:

(a) The BIR, PHILHEALTH, GSIS and HDMF;

(b) Non-stock savings and loan associations and mutual benefits associations duly operating under existing laws and cooperatives which are managed by and/or for the benefit of government employees;

(c) Associations or provident funds organized and managed by government employees for their benefit and welfare;

(d) GFIs authorized by law and accredited by appropriate government regulating bodies to engage in lending;

(e) Licensed insurance companies; and

(f) Thrift banks and rural banks accredited by the BSP.

In no case shall the foregoing deductions reduce the employee’s monthly net take home pay to an amount lower than Four Thousand Pesos (P4,000).

Further, D.O. No. 38, s. 2017 emphasized that all monies due the GSIS and HDMF shall enjoy priority or first order of preference in the salary deductions of concerned DepEd personnel.

In order to improve the financial capability of DepEd personnel, ensure the preservation of their GSIS benefits and fulfill DepEd’s legal mandate under the GAA. the parties agree for DepEd to ensure strict implementation of D.O. No. 38, s. 2017 and for GSIS to extend a financial assistance loan program to DepEd personnel, to be called the GSIS Financial Assistance Loan (GFAL) to DepEd Personnel, to allow them to take out or refinance their outstanding loans with the 213 lending institutions currently accredited with the Department’s Automatic Payroll Deduction System (APDS), through the GSIS.

Based on the partial report submitted by DepEd as of 19 December 2017 covering 85 lending institutions, the total loan receivables of DepEd personnel from the lending institutions stood at Php150,613,881,394.99.

The financial assistance loan program shall be pilot tested in twelve (12) selected cities and municipalities across NCR, Luzon and VisMin regions for a period of six (6) months, to gather and evaluate feedback from both the borrowers and lending institutions and determine the actual potential market for this loan program.

II. OBJECTIVES

- To improve the financial capability of DepEd personnel;

- To provide an affordable loan package to enable DepEd personnel to take out or refinance their outstanding loans with lending institutions through the GSIS; and

- To improve the collection efficiency of GSIS.

III. DEFINITION OF TERMS

| A. Date of Loan Granting | The date when the header corresponding to the loan availed of is created in the IT system of the GSIS. |

|---|---|

| B. Up-to-date Account | A loan account where correct monthly amortization is consistently paid and the outstanding balance is equal to or less than the theoretical balance |

| C. Account in arrears | A loan account with unpaid amortizations equivalent to six (6) months or less. |

| D. Account in default | A loan account is considered in default if the total arrearages or unpaid amortization is equivalent to more than 6 monthly amortizations. |

| E. Theoretical Balance | The balance of the loan if all the monthly amortizations due were paid in accordance with the payment plan or amortization schedule of the loan. |

| F. Outstanding Balance | The sum of the unpaid balance at the end of the month including penalties and surcharges, if any. |

IV. POLICIES

A. COVERAGE

The GFAL to DepEd Personnel shall be exclusive to all active and permanent teaching and non-teaching personnel of DepEd nationwide who have existing outstanding loan obligations with DepEd-accredited lending institutions.

B. GENERAL POLICIES

- The financial assistance loan may be availed for the purpose of settling the outstanding obligations with lending institutions.

- The availment of the financial assistance loan shall be voluntary; hence, shall be extended only to those who will apply for the same.

- The eligible applicant to the loan shall be DepEd personnel.

- The loan proceeds to be paid to lending institution/s shall be net of deductions to be imposed by GSIS, i.e., advance interest payment and loan redemption insurance.

- The lending institution/s should be in the list of accredited lending institutions submitted by DepEd.

C. QUALIFIED LOAN BORROWERS

To qualify for the loan, the Borrower:

- Must be an active regular member of the GSIS with permanent status and paid premiums for the last three (3) years;

- Has no pending administrative case and/or criminal charge: Provided, however, that if the pending case or charge is filed by an accredited lending institution after the issuance of D.O. No. 38, s. 2017 on 31 July 2017 due to the Borrower’s non-payment of his/her loan obligations as a result of the prioritization of GSIS and HDMF loan payments, the Borrower shall remain eligible, subject to the submission of documentary proof stated under Section IV.D of this PPG;

- Is not on leave without pay;

- Has an outstanding loan from DepEd-accredited lending institution; and

- Has no due and demandable loan account/s with the GSIS.

D. APPLICATION

1. Applications for GFAL shall be supported by:

a. Application Form (Annex A) properly filled out by DepEd personnel and duly endorsed by the Authorized Agency Officer (AAO) with borrower’s consent to assign the proceeds of the loan to the concerned lending institution/s.

b. Borrower Loan Agreement, Loan Voucher and/or other certified documents indicating the details of the loan from the accredited lending institution/s, such as: original loan amount, net loan, term of loan, interest rate, monthly amortization and due date of first loan amortization.

c. GSIS pro-forma Statement of Account (SOA) made on the loan issued by accredited lending institution/s with the concurrence of the Borrower as to its correctness (Annex B).

d. Payslips of the borrower for the last three (3) months, certified as true copy by the Authorized Agency Officer (AAO).

e. Such other documents that the GSIS or DepEd may require to verify the balance of existing loan/s with the lending institution/s, and the paying capacity of the borrower.

2. Loan obligations with several lending intitutions shall be consolidated into one application, based on the SOAs to be provided by the same.

E. LOAN AMOUNT

- The maximum loanable amount per borrower is Php500,000, provided that the resulting net take home pay is not lower than the amount required under the General Appropriations Act (GAA), after all required monthly obligations have been deducted.

- The amount set by GSIS as loan amount shall be considered fixed and non-negotiable.

- The arrearages on other GSIS loan/s of a borrower shall not be deducted from the proceeds of the financial assistance loan.

F. TERM

Loan repayment shall be made over six (6) years in seventy-two (72) equal monthly installments.

G. INTEREST RATE

- Interest on loan shall be at six (6) percent per annum computed in advance. The effective rate per annum that shall be used will be 11.258% for 6 years.

- The monthly interest on outstanding balance of the loan shall be computed based on diminishing balance.

- Pro-rata interest covering the days from loan granting up to the end of the month prior to the first due month shall be deducted in advance from the loan proceeds.

The formula for interest in advance (IDA) is as follows:

Interest in Advance (IDA) = GLA x 11.258% x [d(new) / 360]

where: GLA = Gross Loan Amount

d(new) = No. of days from loan granting up to

end of month prior to the first due month

H. REDEMPTION INSURANCE

1. The GFAL to DepEd Personnel shall have redemption insurance (Rl) to safeguard the interests of both the member and the GSIS in case of the former’s untimely death during the term of the loan.

2. The RI rate is as follows.

Loan Term – 6 years

Monthly RI Rate (Per Php1,000 of Loan Amount) – 0.38

3. To ensure that the member is covered with Rl from the date of loan granting, an advance RI premium shall be deducted from the loan proceeds as follows:

| Date of Loan Granting | Rl Premium to be Deducted |

|---|---|

| On or before the 23rd of the month | Equivalent to 1 month |

| After the 23rd of the month | Equivalent to 2 months |

4. If the member dies and the loan is up to date, the loan shall be deemed fully paid by virtue of the RI coverage.

5. In case the loan is in arrears, only the theoretical outstanding balance shall be covered by the Rl benefit and shall be deemed fully paid.

The arrearages, however, shall be deducted from whatever benefits due the deceased. In case the arrearages exceed the benefits due the deceased, the excess shall be deducted from the subsequent benefits due the heirs.

6. In case the loan is in default, the RI coverage shall be deemed lapsed or cancelled. Thus, the outstanding balance at the time of death shall be due and demandable and shall be deducted from whatever benefits due the deceased. In case the outstanding balance exceeds the benefits, the excess shall be collected from the subsequent benefits due the heirs.

7. No RI premiums shall be collected from any benefit that the deceased member and his or her legal heirs are entitled to.

8 The RI is automatically terminated when the member pays the loan in full or upon expiration of the term of the loan, whichever comes first.

I. NO SERVICE FEE

The member availing of the GFAL shall not be charged a service fee by the GSIS.

J. COMPUTATION OF NET PROCEEDS

The net proceeds of the GFAL shall be computed as follows:

| Loan Amount | xx | |

| Less: Interest in Advance (IDA) | xx | |

| Advance Rl Premium | xx | xx |

| Net Proceeds | xx |

K. PAYMENT OF LOAN PROCEEDS

- The loan proceeds shall be paid by GSIS to the authorized representative of the respective lending institutions.

- For this purpose, the name of the authorized representative of the lending institution and corresponding ID number shall be indicated in the SOA to be submitted to GSIS. A copy of the representative’s ID shall be attached to the SOA.

L. MONTHLY AMORTIZATION

Monthly amortization (MA) shall be computed as follows:

where: Amount Borrowed = Gross Loan Amount granted

Annual Interest Rate = 6% nominal, EIR: 11.258%

Term = 6 years

M. DUE DATE OF MONTHLY AMORTIZATION

1. For GFAL loans granted on or before the 23rd of the month, the due month of the first monthly amortization shall be the month immediately following loan granting.

The remittance due date, or the date when the first monthly amortization of the loan shall have been remitted by the agency to GSIS, shall be on or before the 10th day of the month after the due month.

For example:

| Date of Loan Granting | 05 June 2017 |

| Due Month | July 2017 |

| Remittance Due Date Deadline for Remittance to GSIS) | 10 August 2017 |

2. For GFAL loans granted after the 23rd of the month, the due month of the first monthly amortization shall be the 2nd calendar month following the granting of the loan.

The remittance due date shall be on or before the 10th of the month following such due month.

For example:

| Date of Loan Granting | 24 June 2017 |

| Due Month | August 2017 |

| Remittance Due Date (Deadline for Remittance to GSIS) | 10 September 2017 |

N. PAYMENT MECHANISM

1. The monthly amortization shall be paid through payroll deduction. It is understood that the deduction shall not be stopped until the loan is fully paid.

2. The Accounts Management Division (AMD) / Billing, Collection and Reconciliation Division (BCRD) in the CO/BOs shall provide assistance the ERF Handler / Finance Officer in case the Weekly Notice to Deduct (WNTD) and Electronic Billing File (EBF) could not be accessed successfully from the Electronic Billing and Collection System (EBCS).

The EBCS automatically generates email notifications to the ERF Handlers to inform them of the availability of their WNTD and EBF files.

For the EBF files, first notification is sent on the 1st day of the due month, and a second notification is sent on the 15th day of the same due month.

3. Individual accounts whose outstanding balance is equal to or less than P10.00 shall be tagged as “fully paid”. The tagging of fully paid accounts either through direct payment, deduction of arrearages from Enhanced Conso-Loan Plus Program or payroll deduction, shall be done by an authorized officer of the unit/department concerned.

4. The borrower shall directly remit to the GSIS the loan installment as they fall due under any the following instances:

a. The name of a member/borrower is excluded from the monthly collection list;

b. The member-borrower is on secondment, on study leave without pay or extended leave without pay;

c. The monthly amortization is not deducted and/or remitted by the agency for any other reason aside from item 4(b) above;

d. The loan amortization deducted from the payroll is not sufficient to cover the full amount due.

O. PENALTY FOR ARREARAGES

An account is considered in arrears if:

- There is payment for monthly installment but the remittance of said payment is delayed;

- The actual amount paid for the month is less than the amount due for the same month; or

- There is no payment made for the month.

It shall incur a penalty at the rate of 1% per month, compounded monthly, until the arrears are paid.

P. APPLICATION OF PAYMENTS

1. Every payment shall be initially applied to the amount due, following this order of priority:

a. RI premium

b. Penalty, if any

c. Interest

d. Principal

2. If in arrears, the “move-up” policy shall be adopted wherein the payments are first applied to the earliest unpaid month until the month’s full amount due has been fully paid.

3. Lumped repayments whose distributions are indicated in the electronic remittance file (ERF) shall be distributed accordingly and moved-up as appropriate.

Q. AUTOMATIC DEDUCTION OF ARREARAGES

Any and all arrearages from the GFAL shall be deducted from the proceeds of the Enhanced Conso-Loan Plus Program which the borrower may avail of.

R. DEFAULT

An account is considered in default when the total unpaid obligation is equivalent to more than six (6) monthly amortizations.

In the event of default, the outstanding balance of the loan becomes due and demandable without need of demand.

In case of failure to pay the outstanding balance declared in default, the outstanding balance shall be charged with an interest equivalent to 12% per annum compounded monthly (p.a.c.m.) and a penalty of 6% p.a.c.m., from the date of default until the date of full payment.

Any payment received after a loan has been declared in default shall be applied in the order of priority below:

- Rl premiums due for a maximum of six (6) months from the time the account was declared in arrears

- Penalty

- Interest

- Principal

S. PRE-TERMINATION

The loan may be pre-terminated by paying the outstanding balance before the end of the loan term. No fees shall be charged to the borrower in case of pre-termination.

T. COMPULSORY PRE-TERMINATION

The loan agreement shall be deemed pre-terminated upon the death, resignation, permanent disability, retirement or separation from service of the borrower, in which case, the outstanding balance shall be due and demandable and shall be collected by GSIS from claims of borrowers, or their heirs, concerned or by other courses of action (administrative or civil).

Retiring borrowers may opt to avail of the Choice of Loan Amortization Schedule for Pensioners (CLASP), subject to existing policies and procedures.

U. CANCELLATION

Once the loan is approved and the loan proceed is already released to the lending institution/s, the borrower shall no longer have the option to cancel the loan but may only pre-terminate the same through payment of the total outstanding balance.

V. RECOVERY OF AMOUNT IS IN CASE OF MISREPRESENTATION

GSIS shall have the right to declare as due and demandable the total outstanding obligation in case of fraud and/or misrepresentation.

W. REFUND OF OVERPAYMENTS AFTER END OF LOAN TERM

At the end of the loan term, any overpayment shall be treated in accordance with the policy guidelines on treatment of excess payment.

X. NO RENEWAL

The GFAL to DepEd Personnel is a one-time offer of the GSIS and is not renewable.

Y. APPROVING AND SIGNING AUTHORITY ON LOANS GRANTED UNDER GFAL

The certification of availability of funds [Box B in the Disbursement Voucher (DV)] shall follow the limits of authority provided in the existing Manual of Signing and Approving Authorities for miscellaneous transactions.

On the other hand, approval of disbursement of loan proceeds under GFAL shall be as follows:

| Certification (Expense is necessary, lawful, etc.) (Box A in the DV) | Approval (Box C in the DV) | Limits |

|---|---|---|

| Officer I | Dept. Manager III / Branch Manager | Greater than Php400,000.00 up to Php500,000.00 |

| Staff Officer III | Officer I | Greater than Php200,000.00 up to Php400 000.00 |

| Staff Officer I or II | Staff Officer III | Up to Php200,000.00 |

The issuance of checks shall follow the same level of signing authorities for Check as applicable to miscellaneous disbursements processed through the Accounts Payable Module – FIS.

V. DATA AND SYSTEM REQUIREMENTS

A. The Controller Group shall provide the proper accounting entries to record all transactions contained in this PPG.

B. The Operations Groups shall prepare the necessary consolidated user requirements (CUR) and undertake user acceptance testing (UAT) to implement this PPG.

C. The Internal Audit Services Office (IASO) and Information Security Office (ISO) shall review the CUR.

D. The Information Technology Services Group (ITSG) shall ensure that the necessary program for system adjustments is made to conform to this PPG.

VI. INFORMATION DRIVE

The Corporate Communications Office shall prepare the necessary information materials to communicate the implementation of this PPG.

VII. PILOT TESTING

The loan program shall be pilot tested for a period of six (6) months to cover selected teaching and non-teaching personnel of DepEd in twelve (12) selected cities and municipalities across NCR. Luzon and VisMin regions.

The loan program shall be reviewed after the 6-month period for the purpose of determining necessary amendments to the policies and/or procedures, if any, before its nationwide implementation.

The 6-month period shall also provide window for evaluating whether or not the objectives of this PPG are achieved or at least attainable.

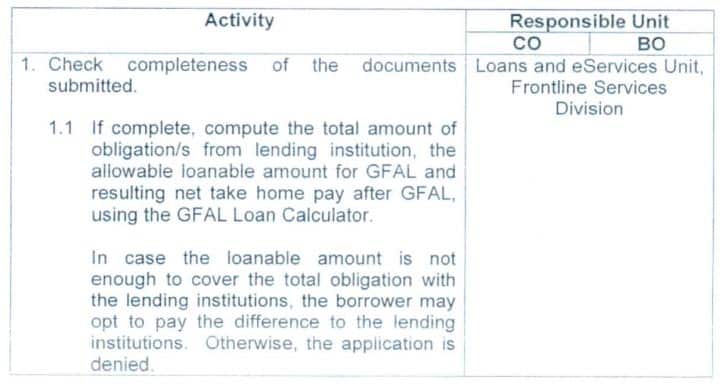

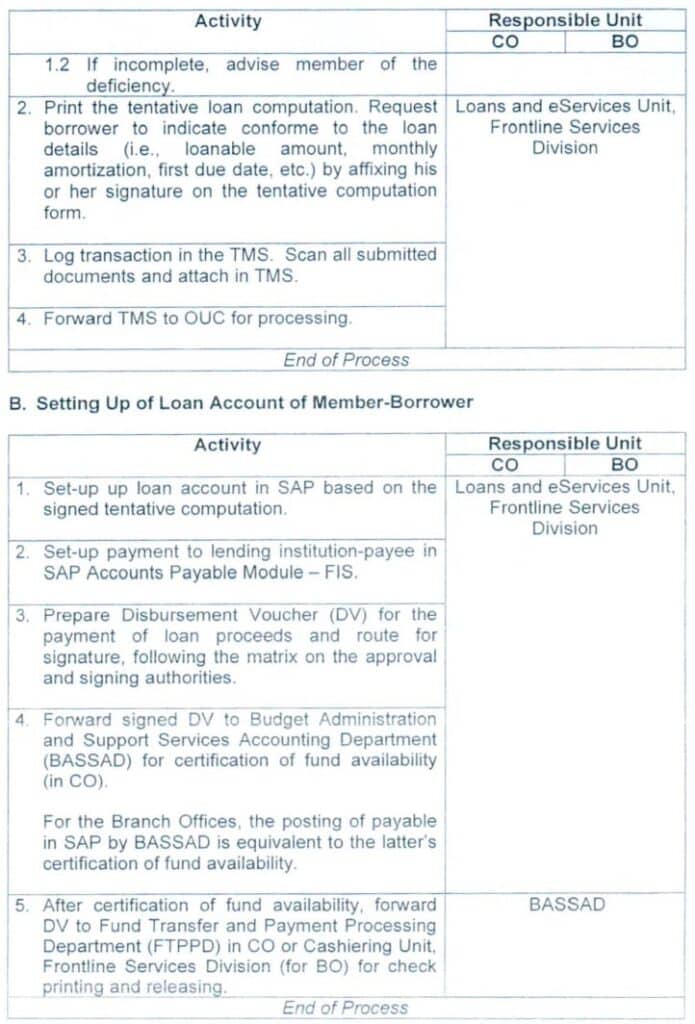

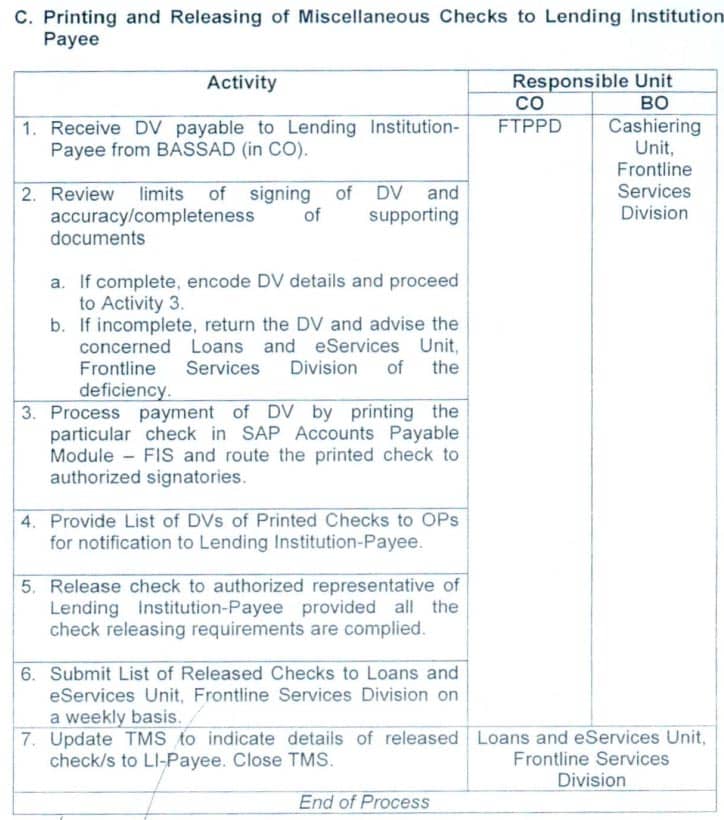

VIII. GENERAL PROCEDURES

A. Evaluation and Acceptance of Loan Application

IX. EFFECTIVITY

This PPG shall take effect after fifteen (15) days from publication in the Official Gazette or in a newspaper of general circulation.

ATTY. JESUS CLINT O. ARANAS

President and General Manager

Hello. What if sobra sa 500, 000 ang loan sa isang PLI, posible pa rin ba yun na matanggap ng gsis at ma grant ang GFAL?

Mgkano po ung monthly amortization ng 500,000 sa gfal?

O

Gustong kong mag gfal, ang offer sa akin ay 440k pwd bang ang maliit na utang ko s isang lending institution lang yong ipa redem ko?

Gusto ko lang po itanong hanggang kailan pwede mag GFAL?

haggang kailan po pwede mag avail nito?

i would like to ask po, kung mag aaply po ng 500,000.00 na GFAL, alam natin ang 6%interest na aabot sa 180,000.00 for 6 yeras, ano naman ang IR na 11.258%? paano siya i cocompute? sa 500,000.00 magkano naman ang monthly amortization? salamat po.

Good evening po. I would like to inquire po sana when will Davao Del Sur or Region XI be able to avail the GFAL Program. Thank you po.

i would like to ask po, kung mag aaply po ng 500,000.00 na GFAL, alam natin ang 6%interest na aabot sa 180,000.00 for 6 yeras, ano naman ang IR na 11.258%? paano siya i cocompute? sa 500,000.00 magkano naman ang monthly amortization? salamat po.

Honestly, I am happy with this GFAL. it’s a great help to all Deped Members event hough I don’t fully understand what read???. Please correct me if I’m wrong, only those who have loans with PLI’s can avail? What about those who don’t have existing loans from PLI’s but have consol loans with GSIS, can they avail GFAL so that interest rates will be lowered from 12% per anum to 6%?